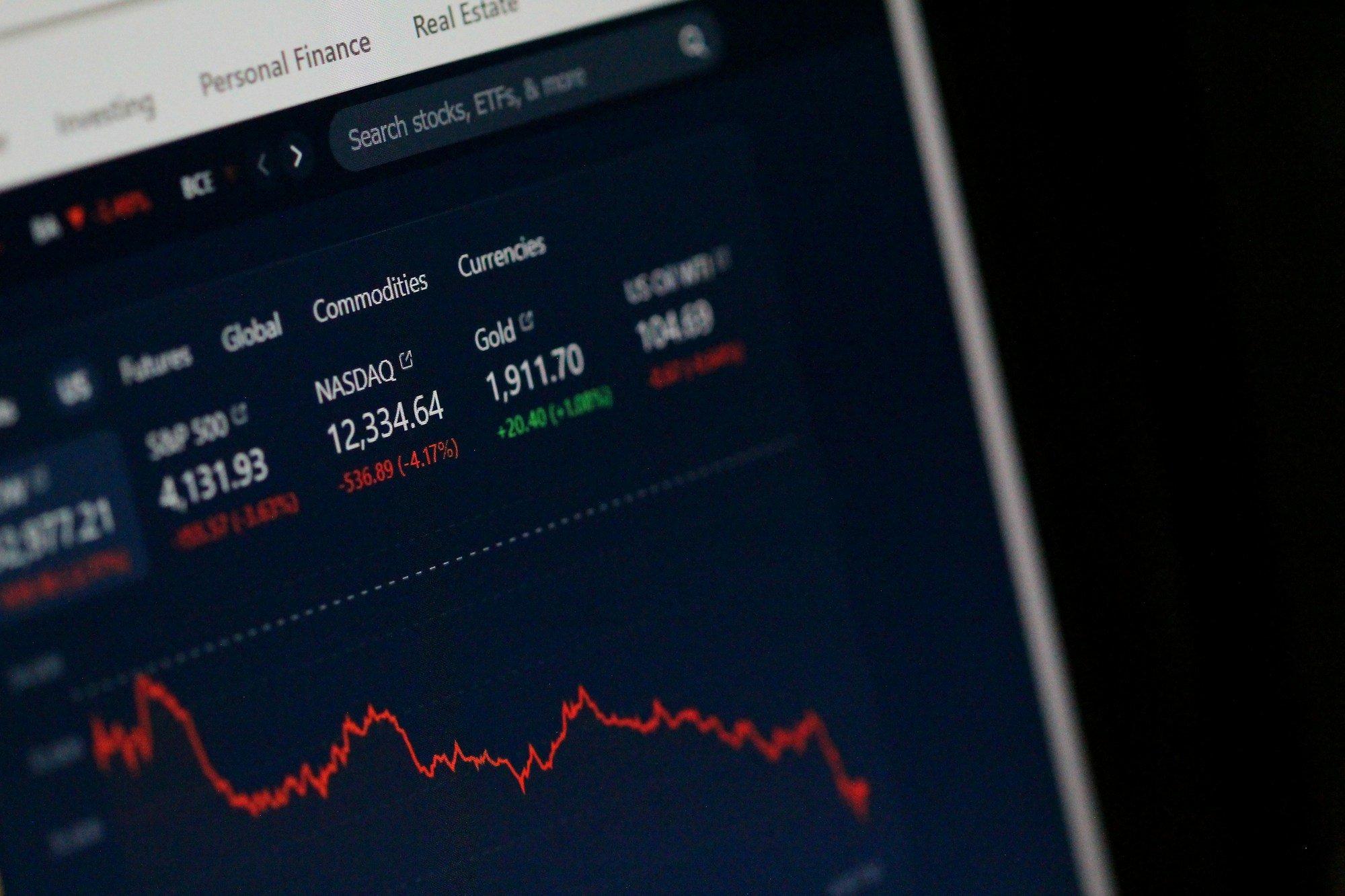

The AI boom that powered Big Tech through much of 2025 is now causing turbulence. Investors are reassessing whether massive capital expenditures on data centers, chips, and generative AI tools will deliver returns fast enough to justify the cost. As a result, shares of Microsoft, Amazon, and Alphabet have come under pressure in recent weeks, while Apple, once criticized for moving too slowly on AI, has quietly outperformed.

After months of celebrating AI-driven growth narratives, analysts across Wall Street are now questioning margin durability, return on invested capital, and whether enterprise demand can sustain the pace of infrastructure expansion. In that environment, Apple’s more measured approach is suddenly looking strategic rather than timid.

Why the AI Trade Is Pressuring Big Tech

- Exploding capital expenditures: Microsoft, Amazon, Meta, and Alphabet have collectively guided toward hundreds of billions in 2026 spending, much of it tied to AI infrastructure and data center build-outs. Investors are concerned that depreciation and operating costs will weigh on margins before monetization catches up.

- Uncertain revenue timelines: While AI tools are widely deployed, questions remain about how quickly they translate into durable subscription growth, pricing power, or new profit streams.

- Valuation compression: After significant multiple expansion tied to AI optimism, even minor earnings disappointments are triggering outsized stock reactions.

- Rising macro risk: Higher-for-longer interest rates and global uncertainty reduce appetite for long-duration growth bets, amplifying scrutiny on speculative spending.

Apple, by contrast, is not committing the same scale of capital to the AI arms race. Consensus estimates suggest its 2026 spending remains far below peers, easing investor concerns about near-term margin erosion.

Hardware Resilience Is Supporting Apple

Despite delays to its next-generation Siri overhaul and a more incremental AI rollout, Apple recently posted stronger-than-expected iPhone revenue. Consumers appear focused on tangible hardware improvements rather than cutting-edge generative AI integration at least for now.

That stability in Apple’s core product cycle is providing a buffer as cloud-heavy peers navigate volatility. However, the company is not immune. Industry-wide memory shortages tied to AI chip demand are pressuring component costs, and executives have signaled that margins could feel that impact in the coming quarters.

The Market Is Becoming More Selective

Reporting from major financial outlets suggests the AI narrative is evolving from broad enthusiasm to stock-by-stock differentiation. Investors are separating companies generating immediate AI-driven returns from those still in heavy investment mode. Nvidia’s upcoming earnings will serve as a key barometer. Strong chip demand could restore confidence in the AI build-out thesis, while any signs of slowing orders could deepen skepticism.

Looking Ahead

The next phase of the AI trade may hinge less on ambition and more on execution. Investors will be watching whether massive infrastructure spending begins translating into sustained earnings growth — and how quickly. Apple’s relative restraint is buying it time, but it will eventually need to prove its AI strategy can compete at scale. For now, in a market wary of overextension, discipline appears to be winning over aggression.